Types of Distributions

7(I)/7(J) Distribution

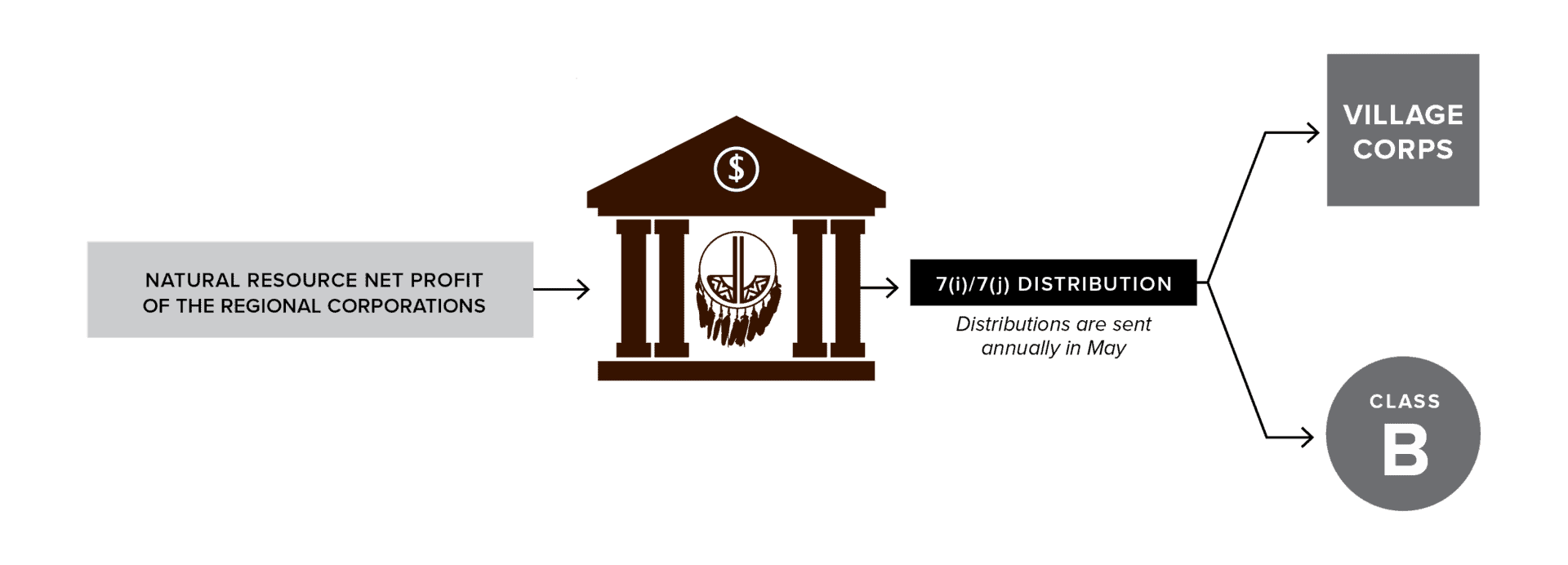

The amount of 7(i) distributions varies depending upon the natural resource net profit of the regional corporations. Doyon receives money from other regional corporations throughout the year. Doyon keeps half the money and deposits the other half in an interest-bearing trust account. That money is then distributed to Class B (at-large) shareholders and village corporations in May.

Doyon Settlement Trust (DST) Distribution

The Doyon Settlement Trust (DST) distribution is a cash distribution. The DST distribution is based upon the number of shares owned by each beneficiary. The amount is based on a five-year average of net income. Beginning in 2019 the

DST distribution replaced the Doyon dividend.

7(I)/7(J) Distribution

Where money comes from and where it goes.

Pursuant to ANCSA

For more information, contact the Records Department at

907-459-2040,

1-888-478-4755

ext 2040, or

records@doyon.com.